Latest update on July 14, 2026

[cg_add-class=heading-style-h4]In a Nutshell

- EFRAG has published an ESRS Data Points List ("EFRAG Implementation Guidance 3 List of ESRS Data Points"; status May 2024), providing an overview over the individual data and related requirements for disclosures

- It encompasses all standards from ESRS 2 and the Topical ESG standards, excluding ESRS 1 General Requirements

- The data points list structures narrative disclosures and is a useful tool when implementing the new standards or conducting a gap analysis

At the heart of the European Sustainability Reporting Standards (ESRS) framework lies a comprehensive and detailed set of data points. These data points are the building blocks of every disclosure — they turn the narrative requirements of the standards into a structured, comparable format.

The Corporate Sustainability Reporting Directive (CSRD) made sustainability reporting mandatory for in-scope EU companies. Two years on, the picture has changed. Wave 1 reporters — broadly the former NFRD population — continue to report under the original ESRS for financial years 2024, 2025 and 2026. From financial year 2027 onwards, only undertakings exceeding EUR 450 million in net turnover AND more than 1,000 employees will be in mandatory scope, under Directive (EU) 2026/470 (Omnibus I). Wave 2 and Wave 3 categories have been deleted.

Understanding the ESRS data points is still essential — for Wave 1 reporters preparing their next statement, for newly in-scope undertakings approaching FY 2027, and for any company using GRI or VSME as the basis for a future ESRS report. This guide walks through the IG 3 list as it stands and flags where the November 2025 EFRAG redraft is changing the shape of the data points themselves.

The IG 3 list dated May 2024 is non-authoritative and accompanies the July 2023 ESRS delegated act, which Directive (EU) 2026/470 is now amending. The , based on EFRAG's December 2025 draft; it applies from FY 2027 (voluntary early use from FY 2026). In short: treat the May 2024 list as a structural reference, not as the final inventory of data points.

Understanding the ESRS Data Points List

The IG 3 list is the most detailed map of the standards as adopted in 2023. It organises every disclosure into rows, with columns describing the related Disclosure Requirements (DRs), Application Requirements (ARs), data type, voluntariness, references to other EU regulation, and phase-in provisions.

The extensive nature of the original ESRS framework is reflected in the tabular ESRS Data Points List, which contains more than 1,000 rows. Each row represents a separable quantitative or qualitative data point and breaks the disclosures down to a granular level.

Gaining a clear understanding of the list of separable data points is crucial to fully grasp the systematic organization of the narrative contents related to the specific “Disclosure Requirement” (DR) or “Application Requirements” (AR).

If you already report your ESG data, this list serves as a foundation for conducting a gap analysis of the existing sustainability information in your company.

Structure of the ESRS Data Points

The ESRS Data Points List is delivered as an Excel workbook with detailed requirements described across columns. It covers all standards from ESRS 2 and the topical ESG standards. ESRS 1 General Requirements is excluded because it does not stipulate specific disclosures.

In the May 2024 list, ESRS E1 (Climate Change) and ESRS S1 (Own Workforce) carry the most data points — roughly 200 each, including MDRs. Note: in the November 2025 EFRAG draft, the per-topic MDRs are being consolidated into ESRS 2 as General Disclosure Requirements (GDR-P/A/M/T). Per-standard counts will look different once the revised standards are adopted.

In the May 2024 workbook, the Minimum Disclosure Requirements (MDRs) are compiled in a separate sheet, "ESRS 2 MDR," with a distinct green background. Each topical standard that has to apply the MDRs has its own line item linking to the relevant requirement.

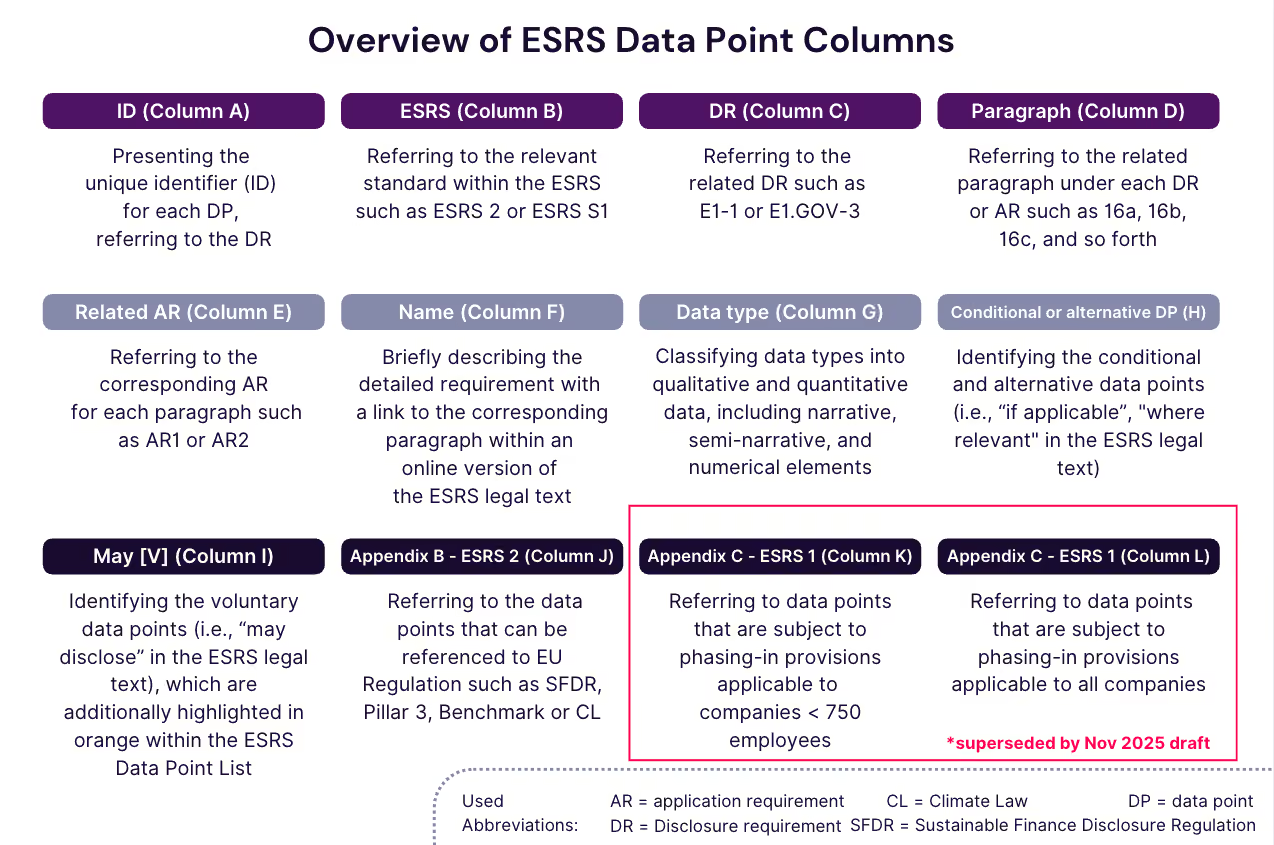

The columns in the Excel workbook are organised as follows. Columns A-J remain valid as a structural reference. Columns K and L are being superseded by the new phase-in provisions in ESRS 1 §125 (more on this below).

- ID (Column A): Unique identifier (ID) for each data point (DP), referring to the corresponding Disclosure Requirement (DR).

- ESRS (Column B): The relevant standard within the ESRS, e.g. ESRS 2 or ESRS S1.

- DR (Column C): The related Disclosure Requirement, e.g. E1-1 or E1.GOV-3.

- Paragraph (Column D): The related paragraph under each DR or AR, e.g. 16a, 16b, 16c.

- Related AR (Column E): The corresponding Application Requirement, e.g. AR1, AR2. Not all data points have specific ARs; some ARs concern the entire DR.

- Name (Column F): Brief description of the requirement (e.g. "Disclosure of transition plan for climate change mitigation"), with a link to the corresponding paragraph in the ESRS legal text.

- Data type (Column G): Classification into qualitative and quantitative data — narrative, semi-narrative, and numerical elements.

- Conditional or alternative DP (Column H): Identifies conditional and alternative data points ("if applicable," "where relevant" in the legal text).

- May [V] (Column I): Identifies voluntary data points ("may disclose" in the legal text). Note: in the November 2025 EFRAG draft and per the Ŕ¶Ý®ĘÓƵ pillar page commitments, the revised standards remove voluntary disclosures. The remaining datapoints are mandatory subject to the materiality filter. The "may" column will become historical context.

- Appendix B - ESRS 2 (Column J): References to data points that link to other EU regulation (SFDR, Pillar 3, Benchmark, Climate Law).

- Appendix C - ESRS 1 (Columns K and L): In the May 2024 list, these columns identify data points subject to phase-in provisions for companies with fewer than 750 employees (K) and for all companies (L). These provisions are being replaced by a new set of phase-ins in ESRS 1 §125 of the November 2025 draft, summarised below.

New phase-ins under ESRS 1 §125 (November 2025 draft)

The November 2025 EFRAG draft replaces the previous phase-in regime with a new one tied to Wave 1 reporters and the reporting period. The most relevant provisions for data-point planning are:

- E4 (Biodiversity & ecosystems), S2 (Workers in the value chain), S3 (Affected communities) and S4 (Consumers and end-users) may be omitted entirely by Wave 1 reporters for financial years prior to FY 2027.

- Anticipated financial effects (ESRS 2 §27 and E1-11) are phased to FY 2027 qualitative / FY 2030 quantitative.

- E2-5 substances of concern: quantitative disclosure phased to FY 2030.

- S1-6, S1-7 (non-EEA workers), S1-10, S1-11, S1-12, S1-13, S1-14: phased to FY 2027.

When the Commission delegated act lands, the IG 3 list will need to be updated to reflect these new phase-ins instead of the 750-employee threshold.

A Closer Look at Data Types

ESRS data points go beyond numbers. They involve a nuanced comprehension of different data types, and a large share of them are qualitative — narrative or semi-narrative format.

Data types in the ESRS Data Points List (EFRAG IG 3, May 2024). Typology preserved in the November 2025 EFRAG draft; Directive (EU) 2026/470 mandates a shift toward quantitative over narrative datapoints.

Data Types:

- Narrative: Descriptive text elements that provide context and qualitative insights; Example: Disclosure of decarbonisation levers and key action‍

- Semi-Narrative: Descriptive elements that can be single text blocks, binary choice (yes/no) or dropdown selections;Â Example: Removals and carbon credits are used [yes/no]

- Numerical: Quantitative elements, for example monetary, percent or volume

Exemplary Numerical Data Types:

- Monetary: Quantifying financial implications of sustainability initiatives; Example from the data point list: "Net revenue used to calculate GHG intensity"‍

- Percent: Expressing proportions and ratios related to sustainability indicators; Example from the data point list: "Percentage of renewable sources in total energy consumption"‍

- Volume: Quantifying tangible quantities relevant to sustainability practices; Example of the data point list: "Total water recycled and reused"

- Energy: Quantifying the unit of energy; Example of the data point list: "Total energy consumption related to own operations"

Mandatory and Voluntary ESRS Data Points

In the May 2024 IG 3 list, voluntary data points are those where the legal text uses "may" instead of "shall." These data points are highlighted in orange in the workbook.

This is changing. The November 2025 EFRAG draft removes voluntary disclosures entirely; the remaining data points are mandatory subject to a materiality filter. ESRS 1 §24 makes the filter explicit:

The undertaking is not required to disclose information prescribed by an ESRS Disclosure Requirement if that information is not material.

In addition, ESRS 1 §27 of the November 2025 draft permits a top-down materiality approach — anchoring materiality in strategy and business model rather than starting from a bottom-up review of every IRO. AR 12 and AR 14 of the same chapter confirm that qualitative analysis can be sufficient and that undertakings do not need to analyse every characteristic of severity or every time horizon.

In short: in the post-revision standards, the question shifts from "Is this datapoint voluntary?" to "Is this datapoint material — and have we documented why?"

Each company still needs to conduct a double materiality assessment to identify the data points relevant for its sustainability statement.

Relation to Digital Reporting (ESRS XBRL Taxonomy)

As of May 2026, mandatory XBRL tagging of sustainability reports is suspended. Directive (EU) 2026/470 amends CSRD Article 29d to provide:

Until such rules on the marking-up are adopted by way of [Delegated Regulation (EU) 2019/815], undertakings shall not be required to mark up their sustainability reporting.

In practice this means:

- Wave 1 reporters preparing FY 2025 and FY 2026 sustainability statements continue to prepare them in single electronic reporting format (ESEF), but are not required to tag the sustainability portion.

- Member States may waive the collective board responsibility for digital marking-up of sustainability information.

- The ESEF Delegated Regulation must be updated before XBRL tagging resumes. The revised ESRS delegated act (adopted 3 July 2026) triggers the ESEF amendment cycle.

- The EFRAG August 2024 draft taxonomy was built against the July 2023 ESRS architecture. Once the revised standards are adopted, the taxonomy will need rework — particularly to reflect the new GDR-P/A/M/T structure in ESRS 2.

Separating the single disclosure items in the narrative text, the ESRS Data Points List is still a useful step for organising sustainability information in a machine-readable way — even outside the suspended XBRL obligation. The structural logic survives the tagging pause. See our dedicated guide on the ESRS XBRL Taxonomy for the full picture.

Practical Insights Into ESRS Implementation

Beyond the regulatory text, the data point list is a strategic tool for sustainability management. Use it to:

- Build a gap analysis against your current ESG reporting (GRI, CDP, EcoVadis, EU Taxonomy).

- Identify which data points are likely to remain after the post-Omnibus revision — those linked to other EU regulation in Column J are a strong proxy.

- Plan the data infrastructure: which data points need primary data, which can use estimates, which are narrative.

- Identify overlaps with VSME (Voluntary SME Standard) for value-chain data collection — important under the new value-chain cap, which limits what large reporters can demand from suppliers with 1,000 or fewer employees.

5 ways ESG software helps you manage ESRS data points

- Start with a gap analysis. Match existing data from GRI, CDP, EcoVadis, EU Taxonomy and other frameworks against the ESRS data points to see where you stand before the revised standards apply.

- Map overlaps once, reuse everywhere. Where ESRS data points overlap with GRI, EU Taxonomy or VSME, map the central information once and reuse it across frameworks.

- Distribute ownership. Assign data points to internal teams and external suppliers; comment and approve at the data-point level.

- Centralise narrative and numerical data with evidence. Keep policies, actions, metrics and targets in one place with the context and proof required for Limited Assurance.

- Track regulatory updates. With the revised ESRS delegated act adopted (3 July 2026), the data points list and assurance expectations will shift. Plan for change.

Ŕ¶Ý®ĘÓƵ's Collaborative Proof Platform enhances accuracy and transparency, and provides a structured workspace for collecting and updating the required data points. With the comprehensive features of the CSRD Module, you can navigate the extensive list of ESRS data points efficiently and stay aligned with the revised standards as they land.

Stop scrambling. Start proving.

Your next customer questionnaire, assessment, or audit doesn't have to be a fire drill. Get the platform that keeps proof ready for every request.

Frequently Asked Questions

A non-authoritative Excel workbook published by EFRAG that breaks down every disclosure in ESRS 2 and the topical standards into separable data points. It accompanies the July 2023 ESRS delegated act. The May 2024 version is the most recent published version; the Commission's revised ESRS delegated act (adopted 3 July 2026, based on EFRAG's December 2025 draft) will trigger a new version.

It is presented in Excel format. Each row is a separable data point; columns describe the related Disclosure Requirement, paragraph, Application Requirement, data type (narrative / semi-narrative / numerical), voluntariness (in the original 2023 ESRS), references to other EU regulation, and phase-in provisions.

Structurally, yes — it remains the most detailed map of the standards as adopted in 2023. But the November 2025 EFRAG draft and Directive (EU) 2026/470 are reshaping the underlying data points: voluntary disclosures are being removed, MDR-P/A/M/T are consolidated into ESRS 2 as GDR-P/A/M/T, the 750-employee phase-in is replaced by new ESRS 1 §125 provisions, and the total count has been cut sharply: the adopted ESRS reduce mandatory datapoints (if material) by roughly 61%, and by around 71% including voluntary datapoints, versus the 2023 ESRS. Use the May 2024 list as a structural reference, not as the final inventory.

It amends the CSRD and the Accounting Directive to (a) raise the mandatory scope to undertakings with >EUR 450 million in net turnover AND >1,000 employees, (b) limit Wave 1 to financial years 2024-2026 and delete Wave 2/3, (c) introduce a statutory value-chain cap and "protected undertakings" concept (≤1,000 employees), (d) suspend mandatory XBRL tagging of sustainability reports, and (e) mandate the Commission to revise the ESRS to remove least-important datapoints and prioritise quantitative over narrative.

The data points list separates each disclosure into a tag-able row, which supports digital reporting in principle. However, mandatory XBRL tagging of sustainability reports has been suspended by amended CSRD Article 29d until the ESEF Delegated Regulation (2019/815) is updated. The EFRAG August 2024 draft taxonomy will need rework before adoption.

Heading

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.